Advanced Market Scanning

Filter thousands of securities with precision using technical and fundamental criteria to spot opportunities fast.

Professional Technical Charting

Customize charts, overlays, and studies across time frames to visualize market movement clearly.

Beyond Charts Formula Language (BCFL)

Turn ideas into strategies with BCFL. A scripting language 99% compatible with MetaStock for advanced analysis.

Realistic Trading Simulator

Test and refine your strategies in live market conditions without risking real capital.

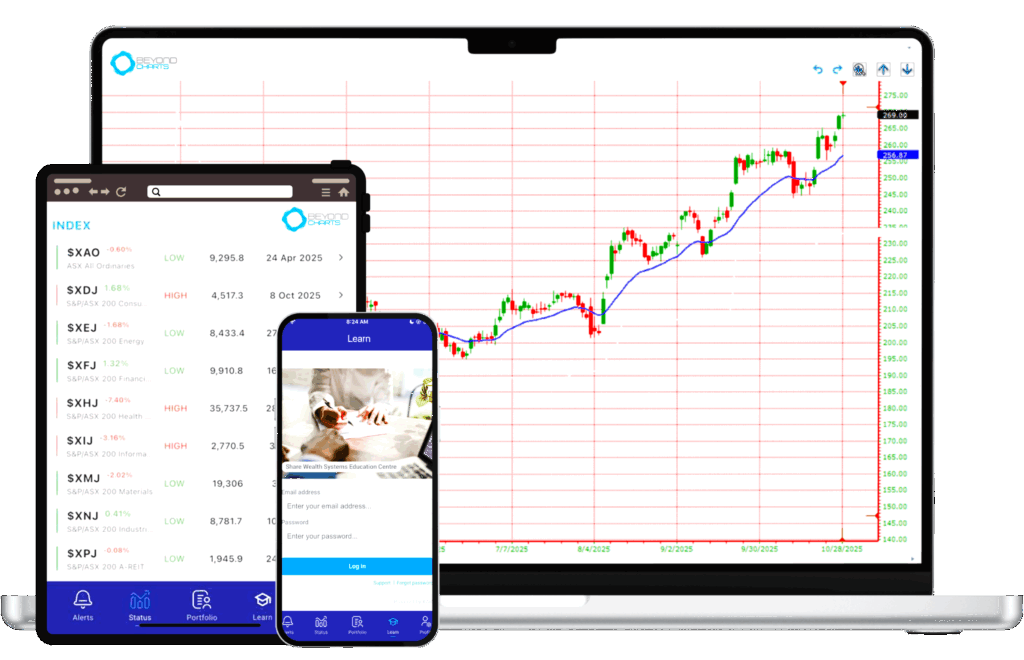

SWS Alerts to Stay Ahead Anywhere

Get real-time buy, sell, or stop alerts on your phone or tablet so you can act instantly.

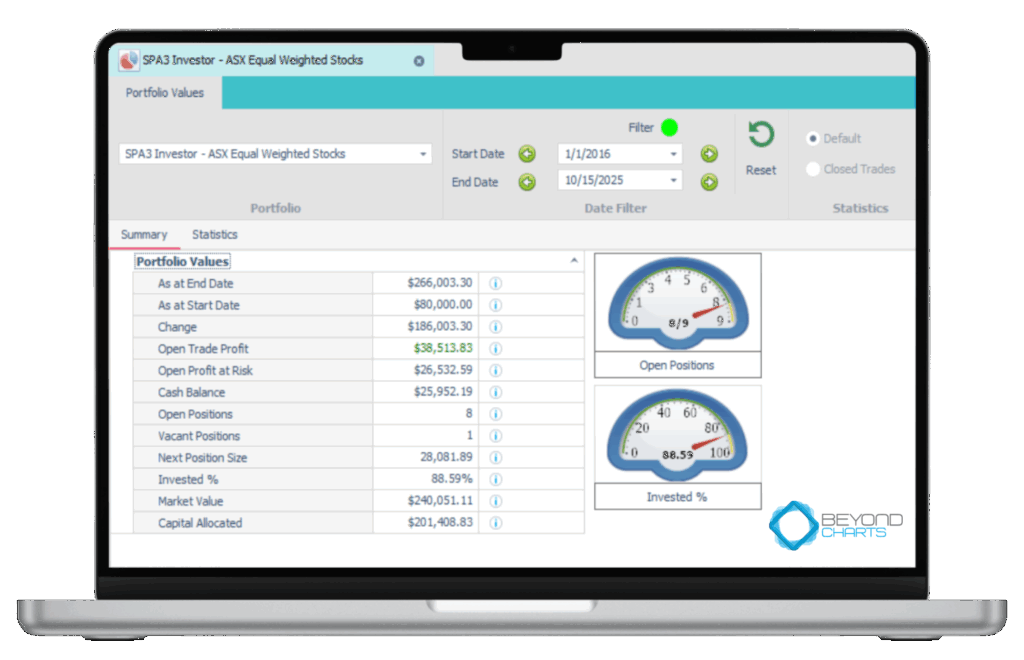

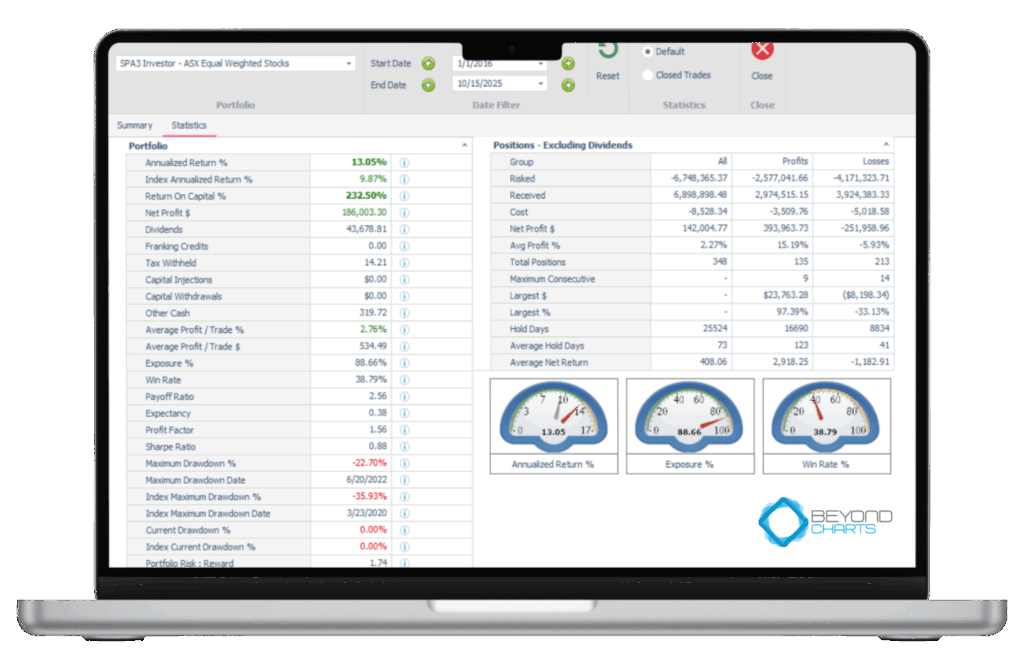

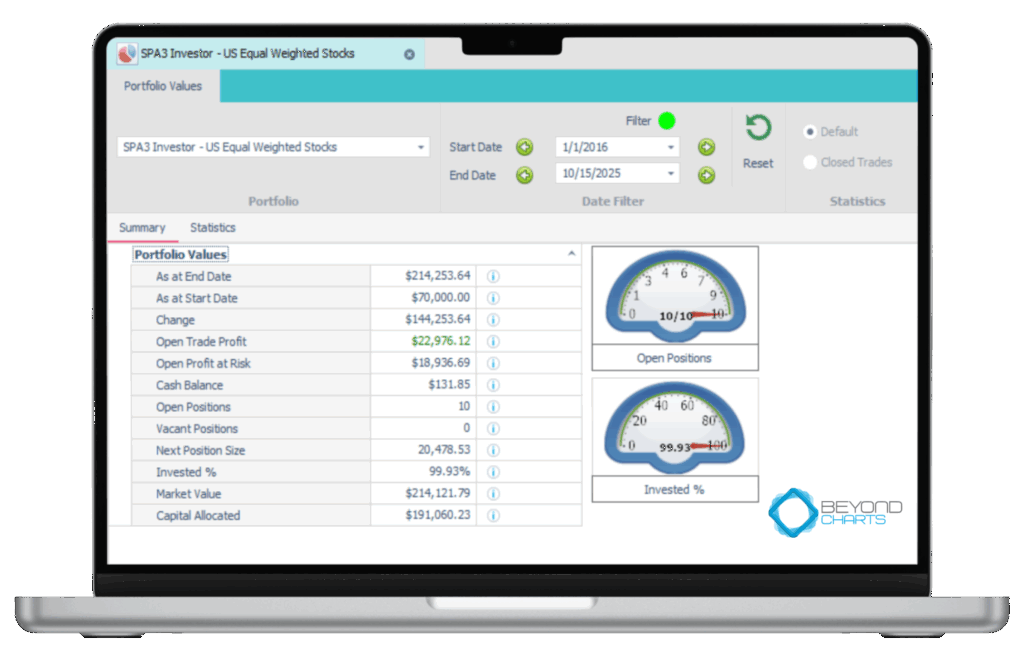

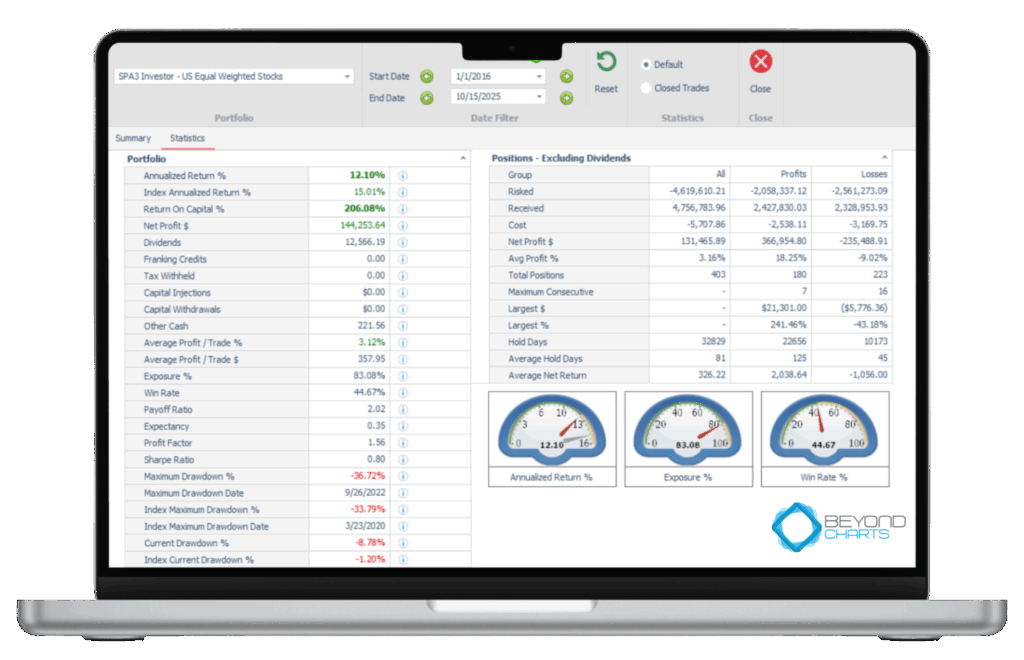

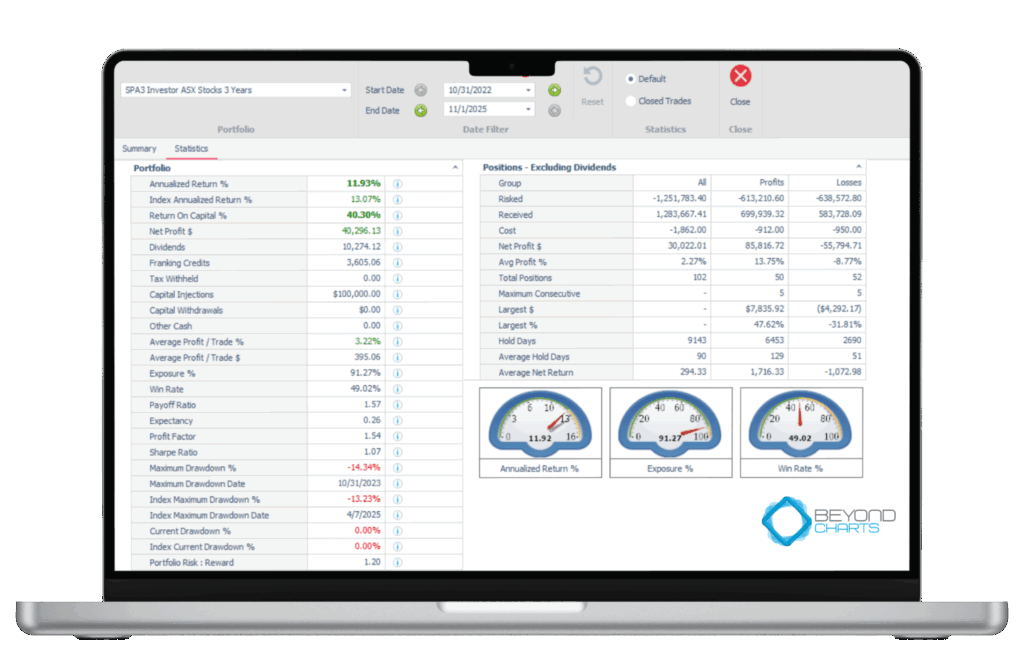

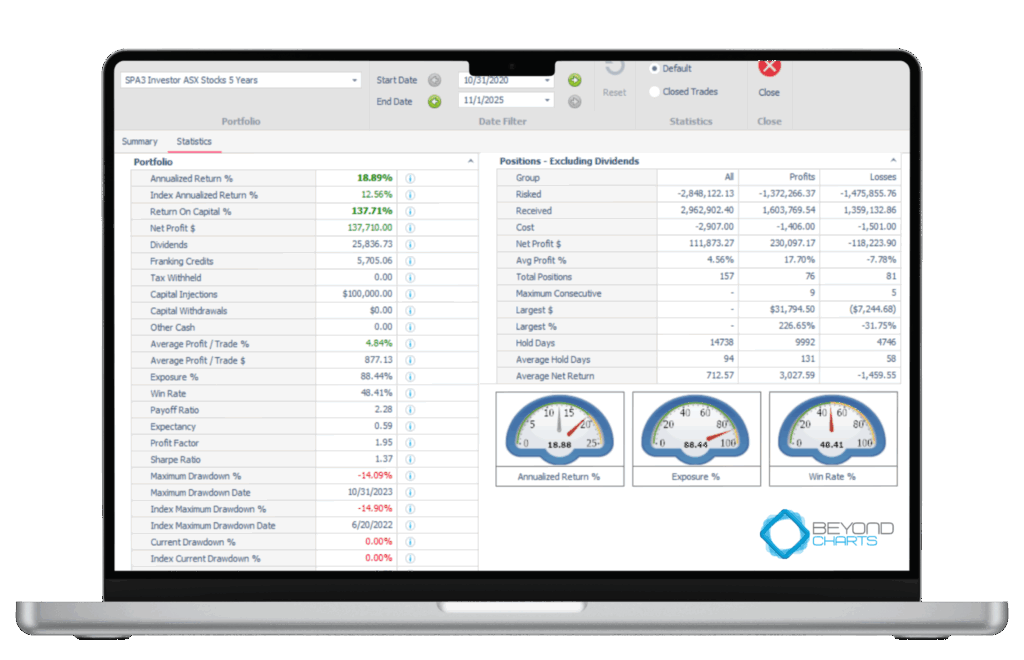

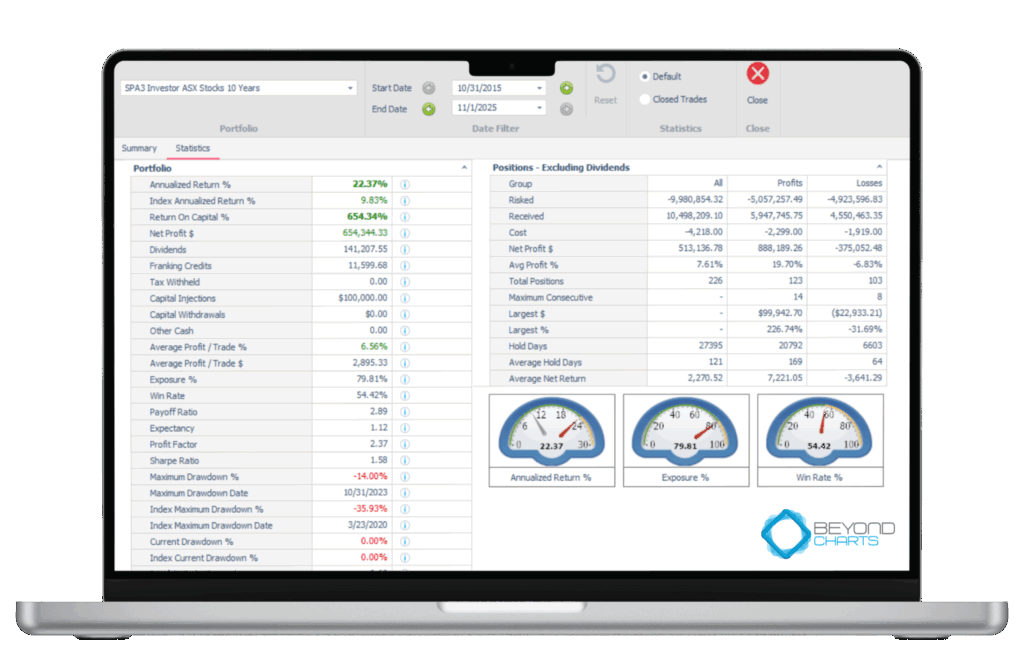

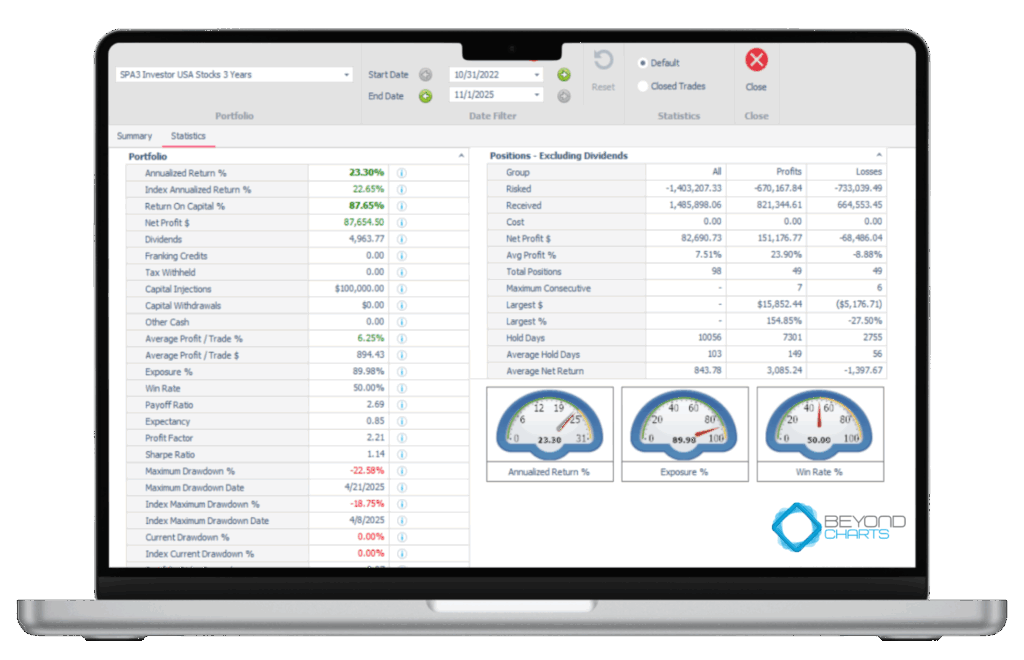

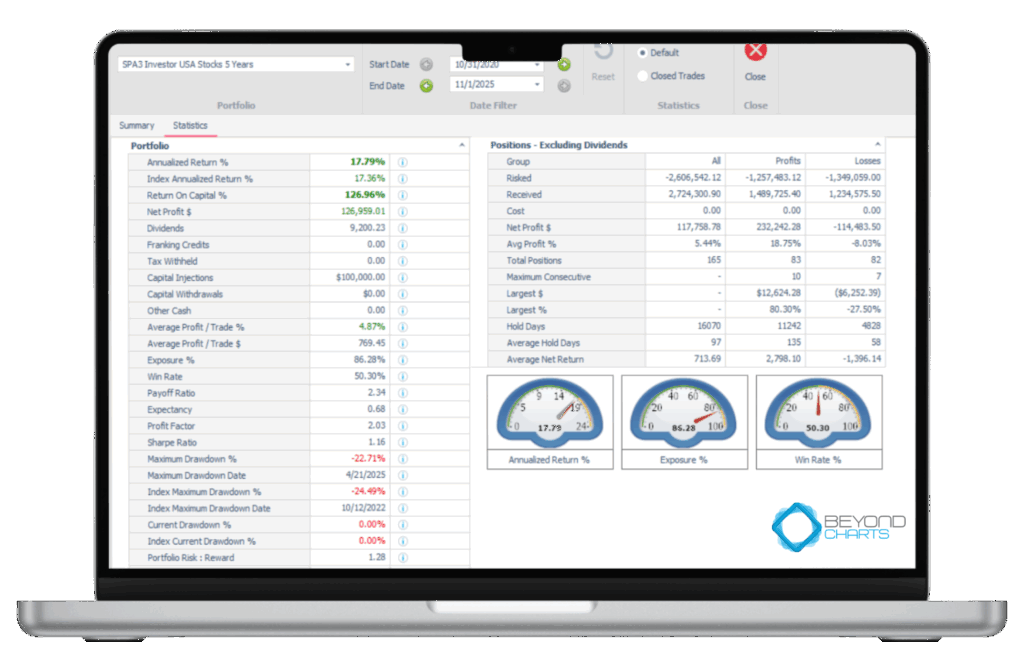

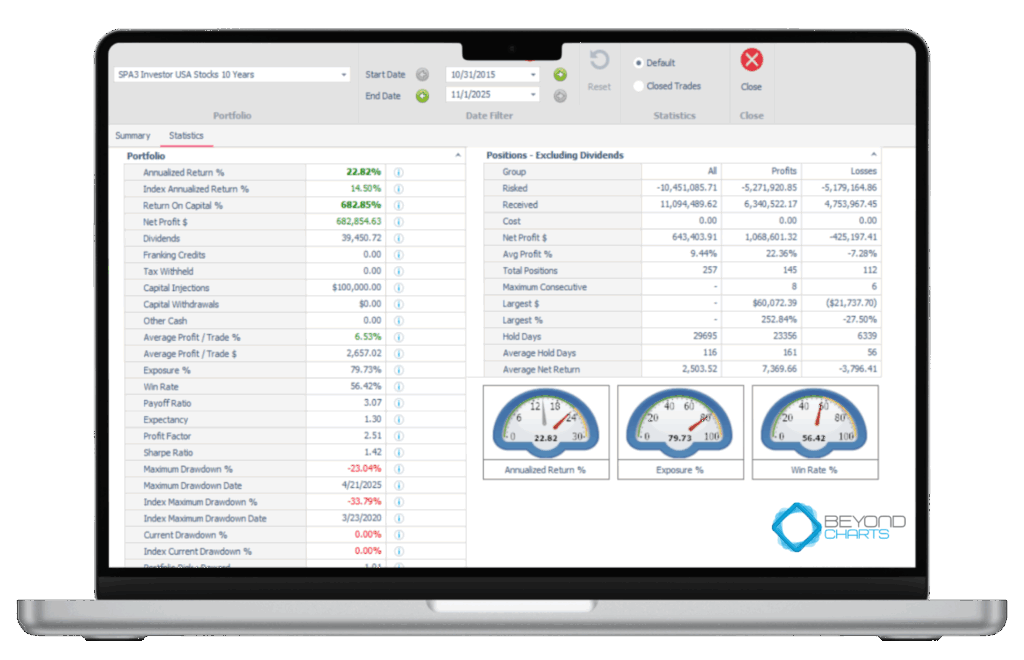

Smart Portfolio Management

Easily track, analyze, and manage both live and paper portfolios in one place.

Watchlist & Workspace Manager

Organize your market view with custom watchlists and saved workspaces that auto-load your preferences.

Data You Can Trust

Rely on premium, accurate market data powering every scan, chart, and backtest.